Like a pot of boiling water

Two years of writing on work and office, and we're still talking about RTO?!

I started this Substack a little over two years ago.

At the time I had some big thoughts I needed to put somewhere:

COVID forever changed the nature of work by making physical location a choice. For the first time, a huge mass of the population could wake up each morning and choose where to work. This was not a choice we had before.

This choice would have far-reaching implications on our personal lives. The relationships we build with our colleagues. The role and significance we ascribe to ‘work’ in our personal identities. The time and care we give to our families, our hobbies, and everything outside ‘work.’ All of these are hugely impacted by where we work: in a lively office in a downtown city center, a bedroom in our family house, a co-working center in Montana.

The ‘right’ choice isn’t easy... Full-time in office is as wrong as fully remote. Workplace relationships matter, and so do commutes.

…and so far we can’t even agree on whose choice it is to make. Employees value workplace flexibility as much as they do healthcare — and so do their bosses. But defining ‘flexibility’ is hard. The right - and completely impractical answer - is to analyze every single activity we do each day and work together when it matters most. Doing that right requires an insane amount of coordination, which most companies are not equipped to handle.

The battle between WFH and RTO is a red herring, a click-baity story that obscures the nuance of this transition. Hybrid is the actual future, so can we just get to that already?

Hybrid would force the office market to undergo a massive shift. Tenants would no longer have fixed requirements (100 people, 100 desks). When the good is a tool, it comes in different shapes, sizes, brands and price points. Office space would no longer be a commodity good. The winners would productize, differentiate, compete. The losers would cover their eyes.

So, two years have passed, and what’s changed?

Shockingly, very little.

Hybrid has clearly won. More than 2/3 of U.S. companies offer workplace flexibility of some kind (i.e., not full-time in person). When you filter out industries like restaurants and food service, education and hospitality, that number is well north of 80%. A full ninety-six percent of tech companies are hybrid.

Office spaces are about as full today as they were two years ago.

Buildings in the average U.S. metro are ~50% as full as they were in March 2020 before the pandemic (which, on average, was 65% utilized — meaning the average building in the U.S. is just a third utilized today).

This is true across regions with little variance. New York and San Francisco are at about equal capacity. The southwest a bit higher, but not by much.

The trend is flat. Based on the underlying data — key card swipes in office buildings — any broad claims that “people are coming back” are baseless. We are about as ‘back’ as we are going to be.

Yet, the misleading WFH x RTO story continues to dominate headlines.

Read the news and you will think we are returning to the office, even though the data tell a different story. There are a few possible explanations for this; the most compelling (and data-backed) is that large companies are using “return-to-office” announcements as a form of backdoor layoffs.

The RTO story is tired.

And the commercial real estate world is loving it.

The office market is not small — $300B+ a year spent on office rent in the U.S. alone. There is a LOT of money tied up in “return-to-office.”

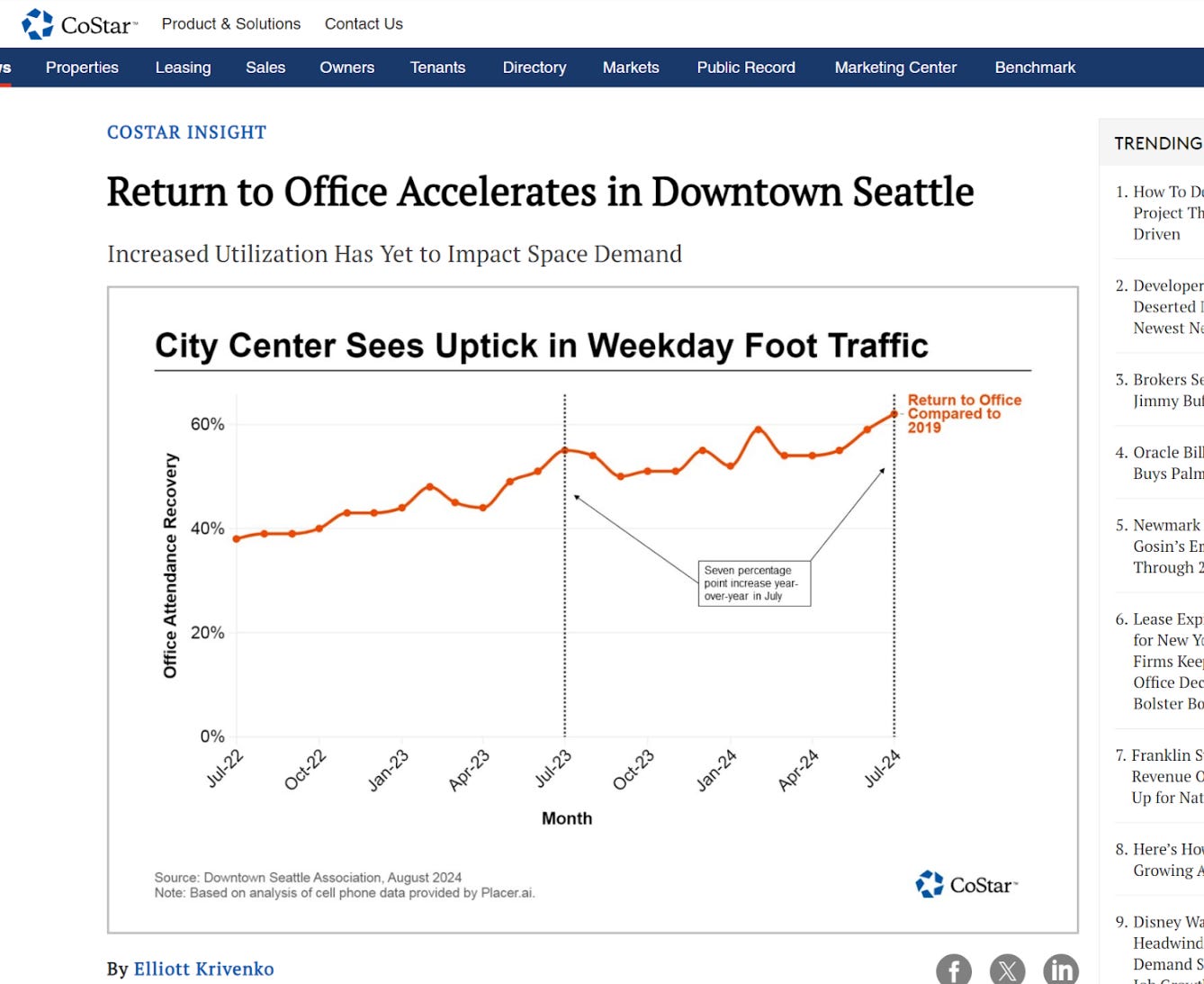

And if you read real-estate news, you’d hardly see the word ‘hybrid’ mentioned. Instead, you’d see a stream of misleading charts and data points that suggest this WILL be the year people return to office. Foot-traffic data has been swapped in for office key card swipe data. The streets are alive and full, so that must mean the offices are back to capacity, right?

In truth, leasing activity HAS picked up. More companies are leasing new office space, as short term COVID-induced lease renewals have started to come to an end.

But the average leased space is 32% smaller than it was before. With smaller spaces and shorter terms, more activity doesn’t mean a resurging market. For that to be true we’d need to see a LOT more activity than we even saw in 2019.

So when does the house of cards collapse?

The answer mostly lies with lenders. CRE loans everywhere have gotten 1 year extensions, in many cases several times over. With broader economic uncertainty still looming, better to blame interest rates and a potential recession than accept a structural change to demand.

That can only last so long.

And I predict that if (as?) interest rates continue to come down and inflation fears settle, the office market nightmare will begin to be accepted as the reality it is.

Not every building will get a headline this drastic, but we will see a lot of keys changing hands:

Lower interest rates will make it clear that the office crisis is not tied to the same financial cycle as today’s residential distress. It is in fact driven more so by a structural change in demand.

It will also allow for much more transaction activity. New owners will swoop in with financing that actually works.

As buildings get ‘reset’ at new bases, new ownership will come in open-minded about change. Without anxious lenders breathing down their necks, and with a new financing stack, owners will see the crisis as an opportunity.

What is that opportunity exactly?

Well, aggregate demand may be falling, but the opportunity to compete and win will be stronger than ever. Tenants will choose the spaces that cater to their needs — not just in build-out, but amenities, services, and flexible terms.

Most owners don’t have the resources or wherewithal to compete. A handful of people who’ve outsourced everything, far away and out of touch with their customer — the tenant.

Those who see the opportunity and not only accept, but invest in change will grow market share and come out stronger than they went into this.

The office will be designed around the TOOL it should be.

And when that happens, the conversation may begin to shift. Dreary RTO headlines will be replaced by stories of new ways of working. Open-mindedness and opportunism will replace denialism.

And then we can finally start talking about all the rest of it — our relationships at work, our identification with work, and the significant choice of physical space.